The Bigger Story Is Not the Loan – It Is What Nigeria Does With It

The World Bank has approved a $1.25 billion financing package for Nigeria under its Nigeria Actions for Investment and Jobs Acceleration (NAIJA) programme, signalling continued international support for the country’s ongoing economic reform agenda despite mounting domestic concerns over its expanding debt profile.

The approval, announced on Wednesday alongside the unveiling of the World Bank’s new Country Partnership Framework (CPF) for Nigeria covering 2026 to 2032, positions job creation and private sector development at the centre of the institution’s engagement with Africa’s largest economy over the next six years.

According to the World Bank, the financing will support policy reforms designed to accelerate investment, improve competitiveness and stimulate employment by strengthening the foundations for sustainable economic growth.

“The World Bank Group has endorsed a new Country Partnership Framework for Nigeria spanning 2026–2032, setting out a strategy to create more and better jobs at scale by unlocking private sector-led growth,” the institution said in a statement.

It added that the newly approved financing operation would support Nigeria’s transition towards a more inclusive economic growth model capable of generating employment opportunities through private sector expansion.

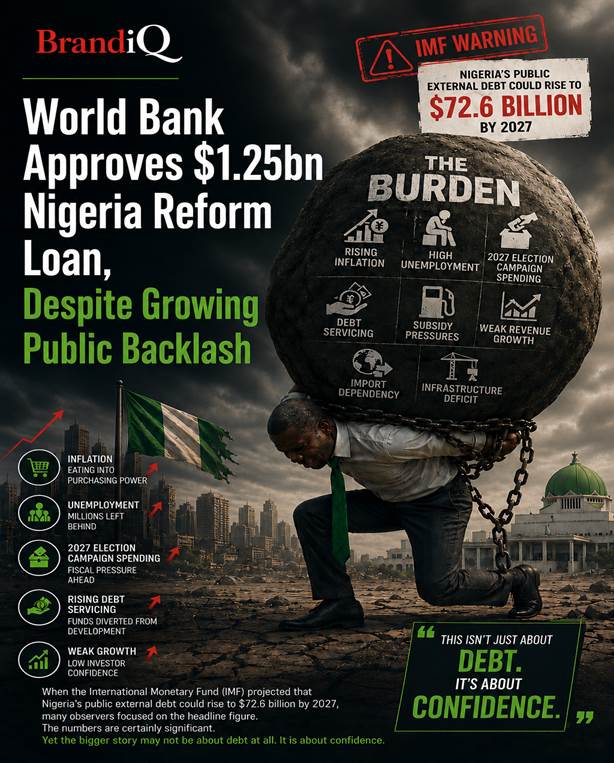

The approval comes amid increasing public debate over Nigeria’s borrowing strategy, with many citizens questioning whether rising external debt has translated into tangible improvements in living standards.

Despite the criticism, the World Bank maintained that recent macroeconomic reforms have strengthened economic fundamentals by supporting stronger economic growth, improving government revenues, increasing external reserves and boosting investor confidence.

Under the new Country Partnership Framework, the World Bank intends to support programmes aimed at expanding electricity access to 32 million Nigerians, providing broadband connectivity for 58 million people, improving health and nutrition services for 40 million citizens, and supporting 9.5 million farmers.

The institution said these interventions are expected to strengthen human capital, improve agricultural productivity and expand access to critical energy and digital infrastructure.

World Bank Country Director for Nigeria, Mathew Verghis, said the institution’s priority would be helping Nigeria convert recent macroeconomic improvements into broader economic opportunities for its citizens.

“Our new Country Partnership Framework provides the strategy for how the World Bank Group will support Nigeria over the coming years, with a strong focus on helping to create more and better jobs, particularly by enabling private sector-led growth,” Verghis said.

He noted that while recent reforms had contributed to macroeconomic stability, sustained improvements in living standards would depend on addressing structural constraints limiting private investment and job creation.

According to the World Bank, the $1.25 billion financing will support reforms in capital market development, digital economy regulation, e-governance, power sector reforms, trade facilitation, agricultural productivity and domestic revenue mobilisation.

Specifically, the institution said the programme would help deepen Nigeria’s capital markets, modernise regulatory frameworks for the digital economy, accelerate electricity reforms, reduce trade barriers in line with Nigeria’s commitments under the Economic Community of West African States (ECOWAS) and the African Continental Free Trade Area (AfCFTA), improve access to quality agricultural seeds and strengthen domestic revenue generation.

The World Bank added that the operation forms part of its broader support for Nigeria through investments in energy, agriculture, digital infrastructure, private sector development and social protection.

Also commenting on the initiative, Dahlia Khalifa, Divisional Director for Nigeria at the International Finance Corporation, said Nigeria’s ongoing reforms have created new opportunities to attract private investment and stimulate employment.

She said unlocking greater investment and productivity would be critical to supporting long-term economic growth in a country with a rapidly expanding population.

Similarly, Ed Mountfield, Vice-President and Chief Financial Officer of the Multilateral Investment Guarantee Agency, said although Nigeria’s reforms have opened new investment opportunities, risks remain for investors.

He explained that MIGA would continue providing guarantees and political risk insurance to encourage private investment in priority sectors, including infrastructure and financial services.

The newly approved facility represents the second-largest single World Bank financing approved for Nigeria under President Bola Tinubu’s administration, behind the $1.5 billion Reforms for Economic Stabilisation to Enable Transformation Development Policy Financing approved in June 2024.

According to figures contained in the World Bank statement, Nigeria owed the institution $17.81 billion as of 31 December 2024. The report also noted that debt to the International Development Association increased from $16.56 billion in 2024 to $18.51 billion in 2025, while exposure to the International Bank for Reconstruction and Development rose from $1.24 billion to $1.38 billion over the same period.

Overall, World Bank loans accounted for 38.36 per cent of Nigeria’s $51.86 billion external debt stock at the end of 2025, according to the figures cited.

BrandiQ Analysis

The Bigger Story Is Not the Loan – It Is What Nigeria Does With It

The approval of another World Bank facility inevitably revives a familiar national conversation about debt, fiscal sustainability and economic development.

For many Nigerians, rising external borrowing has become increasingly difficult to reconcile with persistent inflationary pressures, unemployment and declining household purchasing power. Public concerns therefore reflect a broader demand for greater accountability in the use of borrowed funds rather than opposition to borrowing itself.

However, the World Bank’s latest financing differs from conventional project lending in one important respect. The emphasis is not solely on financing infrastructure. Instead, the programme is designed to support policy reforms intended to make Nigeria’s economy more attractive to private investment.

The reforms outlined under the programme – capital market development, digital economy regulation, electricity reforms, agricultural productivity, trade facilitation and domestic revenue mobilisation – target structural constraints that have historically limited business expansion and investment.

If effectively implemented, these reforms could improve the operating environment for businesses, reduce investment bottlenecks and encourage greater private sector participation in economic growth.

Private Sector Growth Becomes the Central Economic Strategy

Perhaps the most significant feature of the new Country Partnership Framework is its clear emphasis on private sector-led growth.

This reflects an increasingly important shift in development thinking. Rather than relying primarily on public expenditure to drive growth, multilateral institutions are placing greater emphasis on creating conditions that enable businesses, entrepreneurs and investors to generate employment and expand productive economic activity.

For Nigeria, where unemployment and underemployment remain major development concerns, strengthening the investment climate may ultimately prove more sustainable than dependence on government spending alone.

Implementation Will Determine Success

The approval of financing is only the first step. The broader economic impact will depend on how effectively reforms are implemented, how efficiently resources are utilised and whether policy consistency is maintained over time.

The World Bank has outlined ambitious objectives, including expanded electricity access, broadband connectivity, improved agricultural productivity and stronger digital infrastructure. Achieving those outcomes will require disciplined implementation, institutional coordination and sustained policy commitment.

Debt Is Only Productive When It Creates Growth

Ultimately, the debate should perhaps move beyond whether Nigeria should borrow to a more fundamental question: Can borrowed resources generate economic growth sufficient to improve living standards, strengthen businesses and expand employment?

Loans used to finance productive reforms that stimulate investment, improve competitiveness and create jobs have the potential to strengthen long-term economic resilience. Conversely, borrowing that fails to produce measurable economic outcomes risks deepening fiscal pressures without delivering corresponding improvements in national welfare. The World Bank’s latest financing therefore represents both an opportunity and a responsibility.

Its long-term value will be judged not by the $1.25 billion approved today, but by whether the reforms it supports translate into stronger businesses, higher productivity, more jobs and improved living standards for Nigerians in the years ahead.