Why Investors, Businesses and Global Markets Are Watching Nigeria’s Political Economy Closely

Nigeria’s monetary authorities have issued one of their clearest warnings yet about the economic risks associated with the country’s approaching 2027 general elections. The concern is not merely political. It is fundamentally macroeconomic.

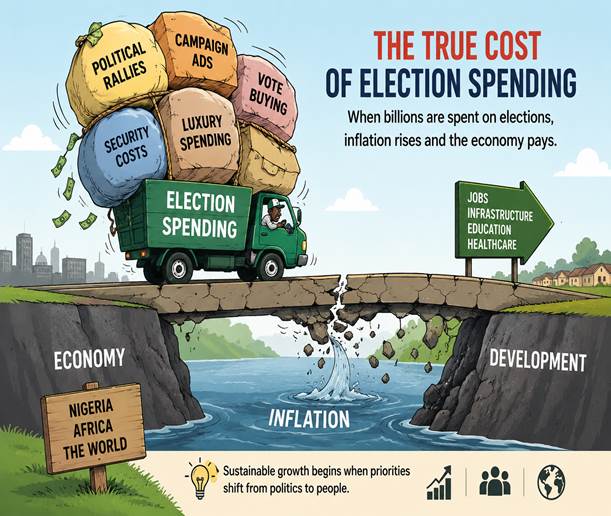

Members of the Central Bank of Nigeria Monetary Policy Committee, MPC, are increasingly worried that rising election-related spending, fiscal injections and politically induced liquidity expansion could reverse the country’s fragile disinflation gains and destabilise broader economic reforms.

Their concern reflects a familiar pattern in emerging economies where pre-election fiscal expansion often collides with monetary tightening efforts, creating inflationary pressures, exchange-rate instability and declining investor confidence.

For Nigeria, one of Africa’s largest economies, the stakes are exceptionally high. The country is attempting to stabilise inflation, restore foreign exchange confidence, attract investment and reposition itself as a major destination for global capital. A politically driven inflation cycle could complicate all those ambitions simultaneously.

The Political Economy of Inflation in Nigeria

Election cycles in many developing economies are frequently associated with increased government spending, patronage networks, campaign financing and liquidity injections into the economy. Nigeria is no exception. Historically, pre-election periods in Nigeria have often triggered higher public expenditure, increased cash circulation, speculative foreign exchange demand and fiscal slippages. These dynamics tend to place pressure on inflation, weaken currency stability and undermine monetary discipline.

What makes the current warning particularly significant is that it is coming directly from multiple members of the Monetary Policy Committee rather than from external analysts alone. That suggests institutional concern within the apex bank about the sustainability of recent macroeconomic improvements.

Although inflation had shown signs of moderation after aggressive monetary tightening, recent data indicate renewed pressure from food costs, transport expenses, accommodation prices and global energy volatility.

Now, election spending risks intensifying those pressures.

Why Election Spending Fuels Inflation

At its core, inflation occurs when too much money chases too few goods and services. Election periods often inject substantial liquidity into the economy through campaign expenditures, government disbursements and politically motivated fiscal expansion. This sudden increase in money circulation boosts consumption demand without necessarily increasing productive output.

In Nigeria’s case, the situation is even more delicate because structural supply-side weaknesses remain unresolved. Agricultural insecurity, logistics bottlenecks, infrastructure deficits, energy costs and foreign exchange volatility continue to constrain productivity. As a result, increased political spending may primarily stimulate prices rather than production.

This explains why the MPC repeatedly referenced “demand-side inflation” and “liquidity surges” in their statements. The concern is not theoretical. It is rooted in Nigeria’s economic history.

Foreign Exchange Stability Could Face Renewed Pressure

Perhaps the most immediate risk concerns the foreign exchange market. Election cycles in Nigeria traditionally increase demand for dollars as political actors, businesses and investors seek currency hedges against uncertainty. Large-scale political financing can also intensify speculative activities within the FX market.

This matters because Nigeria’s recent economic reforms have depended heavily on stabilising the naira and restoring investor confidence in foreign exchange management. If election-related liquidity increases significantly, pressure on the naira could return aggressively. A weaker currency would then transmit inflation across the economy through higher import costs, fuel prices and industrial production expenses.

For businesses dependent on imported raw materials, machinery and consumer goods, this could create another difficult operating environment.

The CBN Faces a Policy Dilemma

The warnings from MPC members also expose a deeper institutional dilemma confronting the Central Bank. On one hand, the economy requires lower interest rates to stimulate investment, private-sector growth and consumer activity. On the other hand, inflationary risks may force the CBN to maintain tight monetary conditions longer than anticipated.

This tension is critical. High interest rates increase borrowing costs for businesses, reduce credit expansion and slow investment growth. Yet premature monetary easing in an election-driven liquidity environment could worsen inflation significantly. The consequence may be a prolonged period of cautious monetary policy. For Nigerian businesses, particularly small and medium enterprises, this means financing conditions may remain difficult well into the 2027 election cycle.

Implications for Nigerian Businesses

The implications for the Nigerian private sector are substantial. Inflation reduces consumer purchasing power, raises operational costs and complicates long-term business planning. Rising transport, logistics and energy costs could squeeze already thin margins across sectors including manufacturing, retail, agriculture and telecommunications.

Businesses may also face heightened exchange-rate uncertainty, making import planning and pricing strategies more difficult. At the same time, investor caution could slow capital inflows into key sectors of the economy. For Nigerian manufacturers, inflationary pressures combined with high interest rates create a particularly dangerous combination because firms face rising production costs while consumers simultaneously reduce spending capacity. This weakens both supply and demand conditions.

Why Global Investors Are Paying Attention

International investors are closely monitoring Nigeria because of its strategic position within Africa’s economic architecture. Nigeria remains one of the continent’s largest consumer markets, a major oil producer and an increasingly important destination for technology, telecommunications, fintech and infrastructure investment.

Macroeconomic instability in Nigeria therefore carries implications beyond its borders. Global investors generally prioritise three conditions in emerging markets: inflation stability, exchange-rate predictability and policy consistency.

Election-driven fiscal expansion threatens all three simultaneously. If inflation accelerates sharply or exchange-rate volatility returns, portfolio investors may reduce exposure to Nigerian assets while multinational firms delay investment decisions pending greater macroeconomic clarity. This is particularly important for investors in the UK, US and Europe seeking long-term exposure to African growth markets. Nigeria’s stability often influences broader investor sentiment toward sub-Saharan Africa.

Africa’s Largest Economy Cannot Afford Policy Reversal

The broader African implication is equally significant. Nigeria’s recent reforms, including exchange-rate liberalisation and tax restructuring, have been interpreted globally as attempts to restore macroeconomic credibility after years of fiscal and monetary distortions.

If election-cycle spending undermines those gains, it could weaken confidence in reform sustainability not only in Nigeria but across African emerging markets. Investors often view Africa through regional sentiment clusters. Economic instability in major economies such as Nigeria, South Africa or Egypt tends to affect capital flows across the continent.

This means Nigeria’s inflation trajectory carries continental significance.

The Global Oil Factor Complicates the Outlook

Another important dimension is global energy volatility. Several MPC members referenced oil price risks because Nigeria remains highly vulnerable to global energy dynamics despite being an oil-producing nation.

Higher global oil prices may increase government revenues, but they also raise domestic fuel and transportation costs under Nigeria’s current market framework. This creates a paradox where oil-price increases simultaneously strengthen fiscal revenues while worsening inflationary pressures domestically. Combined with election-related liquidity expansion, this could complicate monetary management significantly.

Fiscal and Monetary Coordination Becomes Critical

One of the strongest themes emerging from the MPC statements is the urgent need for stronger coordination between fiscal and monetary authorities. This reflects recognition that monetary policy alone cannot manage politically induced inflation effectively. If fiscal authorities expand spending aggressively while the central bank attempts disinflation through tight monetary policy, policy contradictions emerge.

Such contradictions reduce overall policy effectiveness. Nigeria therefore faces a crucial governance challenge: balancing political imperatives associated with election cycles against macroeconomic stability requirements necessary for long-term growth. The success or failure of that balance will shape investor confidence over the next two years.

Implications for UK and US Businesses

British and American businesses with exposure to Nigeria should pay close attention to these developments. Sectors including energy, telecommunications, fintech, consumer goods, banking and infrastructure all depend heavily on macroeconomic stability.

Persistent inflation and currency volatility could affect profit margins, pricing strategies, operational costs and capital allocation decisions. At the same time, periods of economic uncertainty often create selective investment opportunities for firms capable of managing volatility effectively.

Long-term investors may therefore view Nigeria’s current challenges not simply as risks but also as indicators of future structural adjustment opportunities.

BrandiQ Takeaways

The Central Bank’s warning about election-related inflation risks is ultimately a warning about the complex relationship between politics and economics in emerging democracies. Nigeria’s challenge is not merely controlling prices. It is managing the political economy of reform within a high-stakes electoral environment.

The approaching 2027 elections will likely test the resilience of the country’s macroeconomic reforms, institutional coordination and investor confidence. For Nigerian businesses, the message is clear: prepare for prolonged monetary caution, possible exchange-rate volatility and sustained inflationary pressure.

For African markets, Nigeria’s trajectory remains strategically important because the country’s stability influences broader continental investor sentiment. And for global investors, the situation reinforces a central truth about emerging markets: political cycles remain among the most powerful drivers of macroeconomic outcomes.

The next two years may therefore determine whether Nigeria consolidates its reform momentum or re-enters another cycle of inflationary instability.